How to Optimize Your Brand for Social Media Search

By Emily SmithMar 20

Only 25% of marketers truly understand their audience. Do you? Join us for a candid conversation and discover the tools and skills top marketers are using in 2026.

Published April 7th 2026

How is consumer behavior around finances changing?

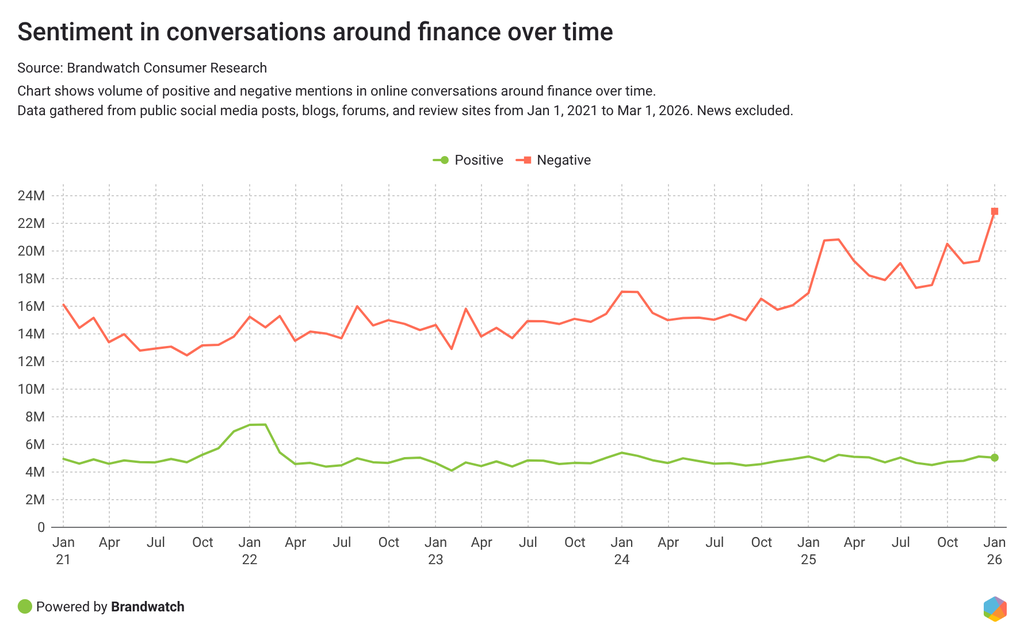

Using Brandwatch Consumer Research, we tracked online discussions relating to finance.

The last five years have shown a clear trend: not only do people talk more about finance – but the conversation is growing more negative. Just in the last year alone (between March 1, 2025 and March 1, 2026), negative mentions grew 21%.

So, what drives this negativity, and how can brands avoid falling out of favor with consumers?

Below, we’ll review some of the biggest themes in consumer conversations around finance, so you can understand your audience better.

Online mentions of “free trials” grew 45% in the past year, and those conversations project plenty of frustration over deceptive and unclear pricing policies.

People share that many apps and services advertise free trial periods but end up charging them immediately after signing up. Others note that reminders are never sent before the free trial converts to a paid subscription.

We tracked 107% more mentions of denied refunds in free-trial conversations. Unclear cancellation policies often lead to charges consumers can’t get out of. Many report that their numerous requests for refunds go unanswered or are flatly denied, leaving them feeling scammed.

The lack of transparency is a huge issue here, and many consumers feel like subscriptions have become a trap.

In our recent State of Social report, we talk about the impact of deceptive pricing tactics on consumer trust. When consumers are charged without their consent, they feel tricked. Many choose not to do business with these brands again, and they make sure to alert others publicly on social media.

Brands looking to maintain credibility with consumers must prioritize consent and clear communication from the beginning. The first impression a brand makes on a consumer often sets the tone for the entire relationship – or ends it before it begins.

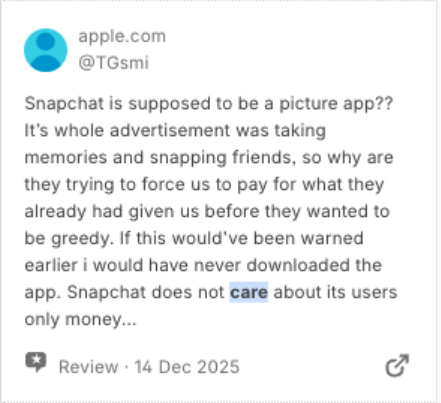

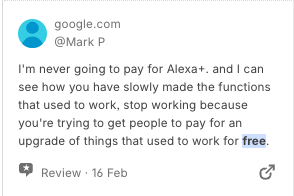

Across industries, brands are quietly removing free perks and replacing them with paid options. And consumers aren’t happy.

Earlier this year, Bilt credit card made significant changes to how points can be earned, replacing the only requirement (five transactions per month) with a more complex system. It didn’t go down well with the Bilt audience – many of them took to social media to explain the math behind why they are no longer interested in this credit card.

And Bilt isn’t the only one. Mentions of downgrades and removal of benefits rose 19% over the past year. Revoked or replaced benefits have created plenty of frustration across industries – from social media platforms introducing premium features to gaming consoles and buy now pay later (BNPL) services.

Consumers don't want to be pushed to pay for what was once free, and some are confused over new benefit systems. But most importantly, people feel betrayed by what they see as broken promises, viewing these changes as companies prioritizing profit over their loyalty.

Brands need to remember to manage change when they've already built loyalty. Before pulling benefits consumers have come to rely on, brands should give excess notice and keep customer education in mind to give their userbase time to adjust.

Remember, loyalty works both ways.

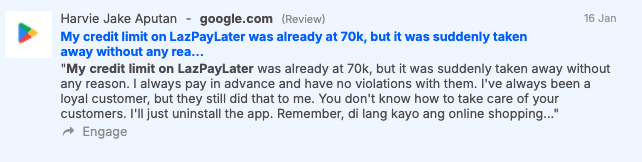

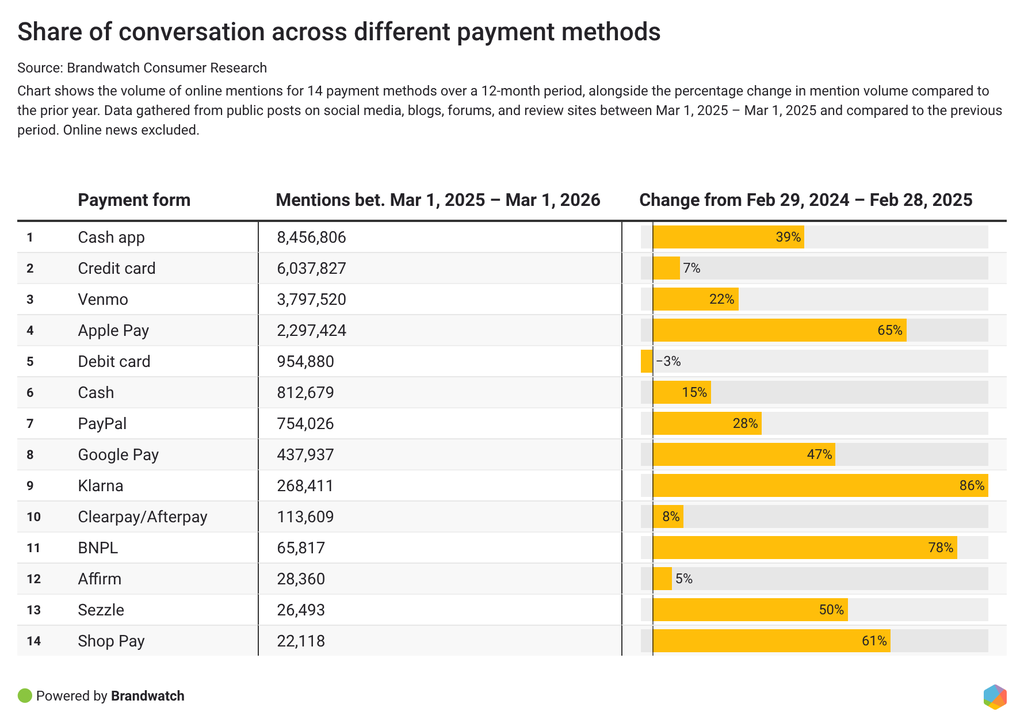

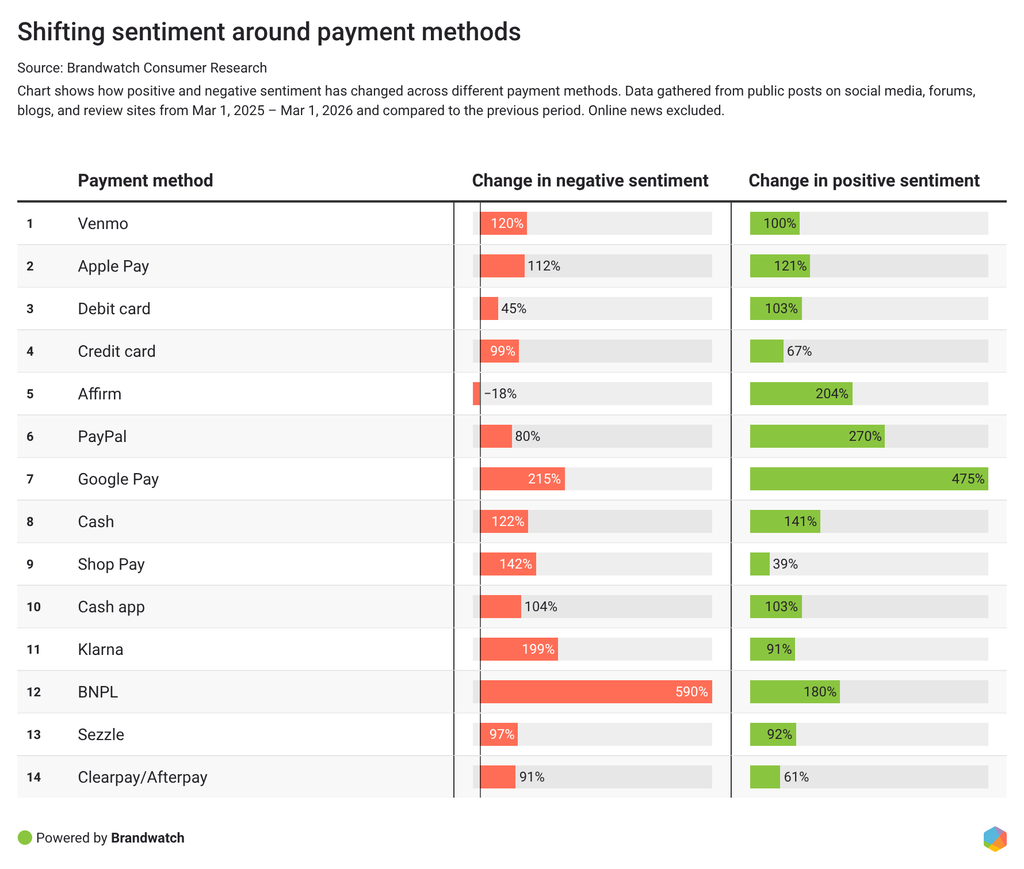

Across 14 different payment methods, Klarna and buy-now-pay-later saw the largest increase in the volume of mentions – up 86% and 78% from the previous year, respectively.

BNPL’s negative sentiment also skyrocketed almost 600%.

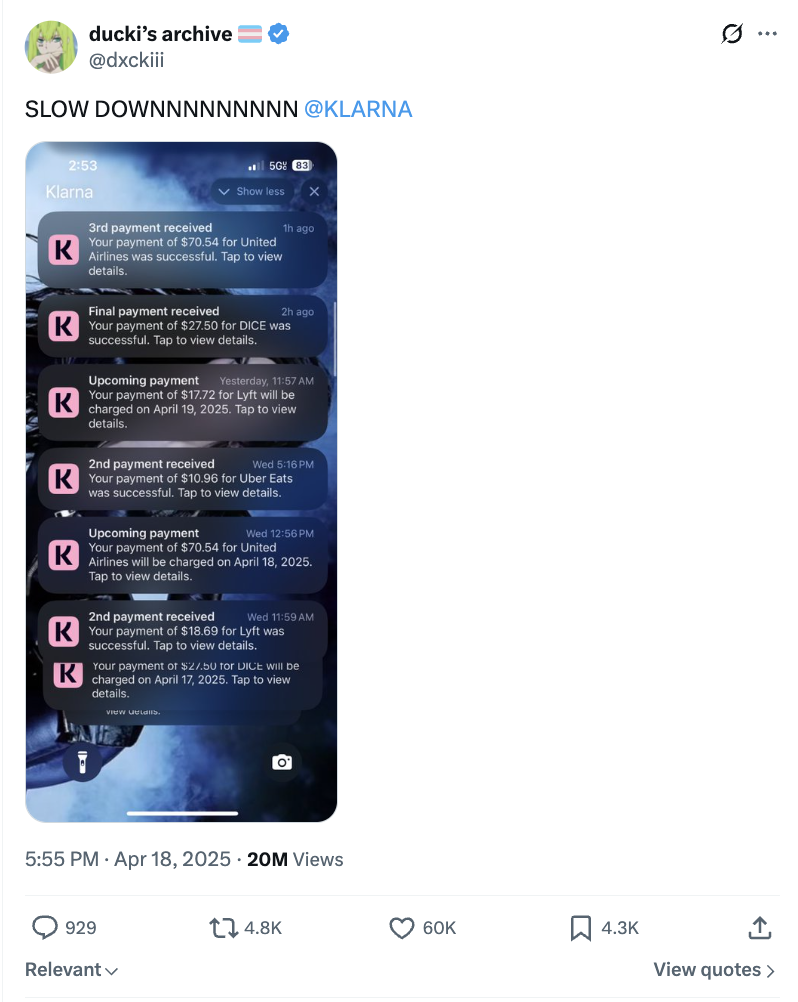

So, what’s triggering negative discussions relating to BNPL?

BNPL helps consumers break down payments over time. It takes the pressure off paying purchases all at once. And spreading payments across actually often pushes consumers to spend more.

The benefit – ease of making purchases – that comes with BNPL payment platforms has a drawback – overspend – that’s putting a strain on consumers’ budgets and mental health.

Many people report feeling trapped in a cycle of debt and struggling with repayments, leading to increased financial stress and potential long-term consequences. Online conversations indicate that many consumers may not fully understand the implications of their borrowing on personal finances, particularly for younger generations who may lack experience in managing credit.

This trend raises questions about financial literacy and responsible spending, as consumers might overlook the long-term impact of accumulating debt.

Brands in finance services need to continue to educate consumers on how to handle personal finances and how impulsive purchases can lead to financial instability. Those brands that do a great job in helping their customers make informed financial decisions will stand out as partners, not just payment providers.

This analysis is based on 609 million online conversations over a 12-month period, pulled from social media, forums, review sites, and blogs with the help of Brandwatch Consumer Research.

We looked at key themes in conversations about finance to understand where consumer expectations are heading.

Looking to dig deeper into finance trends that matter to your brand?

With Brandwatch Consumer Research, you can zoom in on what matters to your business:

Consumer Research gives you access to deep consumer insights from 100 million online sources and over 1.4 trillion posts.

Existing customer?Log in to access your existing Falcon products and data via the login menu on the top right of the page.New customer?You'll find the former Falcon products under 'Social Media Management' if you go to 'Our Suite' in the navigation.

Brandwatch acquired Paladin in March 2022. It's now called Influence, which is part of Brandwatch's Social Media Management solution.Want to access your Paladin account?Use the login menu at the top right corner.